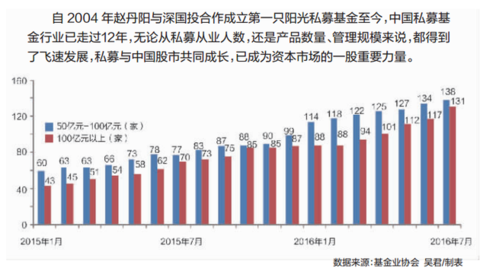

Sina Fund Exposure Desk: The letter is lagging behind false propaganda, the performance is lower than similar products for a long time, what should I do if the fund is pitted? Click [I want to complain], Sina will help you expose them! The birth and development of China's private equity funds February 20, 2004 Private equity investor Zhao Danyang cooperated with SZI Trust to establish the “Shenguotou-Zhizi Heart (China) Collective Fund Trust Planâ€, which was regarded as the first private private equity product in China by the industry and opened in the form of “investment consultantâ€. The pattern of private equity fund sunshine. 2006~2007 The first wave of public fund managers to switch to the private equity industry has emerged, including heavyweights such as Xiao Hua, Jiang Hui, Zhao Jun, Tian Ronghua, and Xu Dacheng, who have “smuggled†and brought new investment ideas and methods. January 23, 2009 The China Banking Regulatory Commission issued the "Guidelines for the Operation of Trust Companies' Securities Investment Trust Business", becoming the first document to regulate securities trust products, which means that the private equity model of the Sunshine has been regulated for many years. Year 2009 The second wave of "public and private" booming, the public fund managers such as Zeng Zhaoxiong, Sun Jiandong, Xu Liangsheng, Li Wenzhong, Li Xuli, etc., all switched to private placements this year, and the industry continued to grow and develop. December 7, 2009 Xu Xiang, a Ningbo-born traveler, came to Shanghai to set up Zexi Investment and issued Zexi Ruijin No. 1. On November 1, 2015, Xu Xiang was suspected of insider trading, manipulating the market and other illegal and criminal acts, and was taken by the public security organs in accordance with the law. 2012~2015 The original "public recruitment of a brother", Huaxia Fund Wang Yawei left, South China Fund Investment Director Qiu Guolu resigned, marking the third wave of "public and private" boom. A large number of public fund managers such as Wang Ruyuan, Wang Penghui, Lu Yizhen and Wang Weidong joined the private equity industry with the arrival of a new round of bull market, and “public and private†reached a climax. December 28, 2012 The National People's Congress passed the newly revised "Securities Investment Fund Law" and added the "non-public fundraising fund" section to make provisions on private equity funds, which means that the legal status of private equity funds has been established and become a regular army. December 2013 Private equity godfather Zhao Danyang believes that A shares have reached the bottom of the value and announced their return to the market, issuing the first product “China Resources Trust – Red Heart Value Collection Fund Trust Planâ€. January 17, 2014 China Securities Investment Fund Association issued the "Private Investment Fund Manager Registration and Fund Filing Procedures (Trial)", opened the private equity fund filing system, and granted the legal status of private placement. At the same time, private placement as a manager can independently issue products. March 2014 The fund industry association issued the private fund manager registration certificate for the first batch of 50 private placement institutions. The qualified private placements can engage in private equity investment, equity investment, venture capital and other businesses and become regular troops. June 30, 2014 The CSRC reviewed and approved the Interim Measures for the Supervision and Administration of Private Equity Funds. On the basis of the filing system, it further made comprehensive provisions on the regulation of private equity funds, including Sunshine Private Equity. February 2016 to present The fund industry association has successively issued the "Guidelines for Internal Control of Private Equity Investment Fund Managers", "Measures for the Management of Information Disclosure of Private Equity Investment Funds", and "Regulations on the Management of Private Investment Fund Raising Behaviors" and other private industry self-discipline rules, and issued "Regulations on Further Regulating Private Equity Fund Management" Announcement on the registration of certain matters, and from November last year, eight batches of lost private placements were announced. The association hopes to build a self-regulatory rules system for the private equity industry and regulate the development of the private equity industry. The status quo of private equity industry development 1. Number and performance of private equity products 1. The number and scale of private equity offerings over the years Wind data shows that as of August 22, 2016, since 2004, the number of private equity products has increased from 47 to 7,565, and the scale of product issuance has increased from 789 million yuan to 59.978 billion yuan. Especially in the two rounds of big bull market in 2007 and 2015, private equity followed the market and grew rapidly in terms of product quantity and scale. In 2015, the number of private equity products was 17,869, with a scale of 223.754 billion yuan, the highest in the calendar year. 2. Private equity performance According to the national gold data, from the end of 2011 to June 2016, the private equity fund in the whole market performed better than the CSI 300 index, but weaker than the CSI 500 index, and the overall absolute return was relatively high. Second, the status quo of private equity fund filing 1. Status of private equity fund management registration From January 2015 to January 2016, the number of private equity fund managers registered with the fund industry associations increased steadily, from 6,974 to 25,841, an increase of nearly three times, implying the rapid expansion and development of private equity funds. After the "Announcement" on February 5, the Association requested that the registered private placement manager need to file the first product. Otherwise, the registration of the administrator will be cancelled. Since April 2016, the number of private placement managers has decreased, and the first phase of cleanup in May will be completed. In the “empty shell†private placement operation, 2,000 private placements were cancelled. By the second phase in August, more than 7,800 private placements were cancelled. More than 10,000 private placements were cancelled in the above two stages. The number of private placement managers has dropped to 16467. Family. After the "Announcement" on February 5, some private placements took the initiative to cancel the manager's qualifications, and at the same time, new private placements were completed under the new regulations, with more than 900. 2. Private equity fund filing status and scale From January 2015 to July 2016, the number of private equity products registered increased from 8846 to 36,829, an increase of more than three times. This means that more and more private placements will record their products, regulate their operations, and privately raise products. As the market trend of A market shows a different growth trend. In particular, after the publication of the "Announcement" on February 5, 2015, the number of private equity fund filings broke out after requiring the registered private placement to file the first product. From January 2015 to July 2016, the asset management scale of private equity funds increased from 2.63 trillion yuan to 7.47 trillion yuan, nearly doubled. The total size of private equity management can be comparable to that of public offerings. 3. Status of employees in the private equity industry From January 2015 to June 2016, the number of private equity workers increased from 124,400 to 40,200, an increase of more than 2 times, indicating that more and more people are entering the private equity industry, and there are also many public fund managers with the market. "Public and private." Especially in November 2015 and March 2016, the number of private sector employees suddenly exploded, which may be related to market conditions and supervision. The sudden drop in the number in July 2016 may be related to the clearance of private shells. 4. Status of private placement As a benchmark for the industry, private equity funds with a management scale of 5 billion and more than 10 billion have received much attention. From January 2015 to July 2016, the number of private placements from 5 billion to 10 billion yuan has increased from 60 to 138. 1.3 times, and the number of private placements with a management scale of more than 10 billion yuan has increased from 43 to 131, a two-fold increase, but the management scale of most private placements is still very small. 5. Securities private placement status From January 2015 to July 2016, the number of securities private placement managers increased from 2,527 to 7,609, a two-fold increase, due to the decline in the number of private shells, and the number of private equity funds registered from 4,383 The growth to 21,948 only increased by 4 times; while the scale of securities private placement management increased from 850.6 billion yuan to 237.11 billion yuan, an increase of nearly 2 times. Supervision of private equity funds 1. Securities Investment Fund Law (Amended in 2015) The National People's Congress passed on December 28, 2012 Key points: Non-public fundraising funds should be raised to qualified investors, and the number of qualified investors must not exceed 200. Significance: For the first time, non-public fundraising funds (private funds) are included, which means that private equity investment funds have obtained legal status. 2. "Private Investment Fund Manager Registration and Fund Filing Procedures (Trial)" Promulgated by the Fund Industry Association on January 17, 2014 Key points: (1) The private placement manager shall perform the registration procedures of the fund manager and apply to become a member of the association. (2) The private placement manager shall file the product after the completion of the fundraising. (3) The registered private equity fund may apply to open a securities related account. Significance: The "Measures" stipulates the specific requirements for private placement filing, which means that the fund industry association officially launched the private equity fund registration and filing work, clarifying that the private equity fund does not adopt administrative approval but the filing system, thus opening the prelude to the private placement filing. 3. Interim Measures for the Supervision and Administration of Private Equity Investment Funds Reviewed by the China Securities Regulatory Commission on June 30, 2014 Key points: On the basis of the filing system, the Measures further comprehensively regulate the regulation of private equity funds including Sunshine Private Equity, including the definition of private equity funds, self-regulation of private equity by associations, full-caliber filing system, and qualified investor system. Basic rules and rules for private equity funds such as fundraising rules and investment operating rules. Significance: It means that the private equity industry has officially established a clear regulatory approach, which has been incorporated into the regulatory system, and the industry has begun to move toward a standardized development path. 4. "Guidelines for Internal Control of Private Equity Fund Managers" Promulgated by the Fund Industry Association on February 1, 2016 Key points: The Internal Control Guidelines are internal norms of private equity firms, which run through private fund raising, investment research, investment operations, operational guarantees and information disclosure. Significance: To ensure the legal and compliant operation of various businesses, to achieve business objectives and to ensure the security of private equity funds. 5. "Management Measures for Information Disclosure of Private Equity Investment Funds" Promulgated by the Fund Industry Association on February 4, 2016 Key points: The “Publishing Measures†imposes normative requirements on private information disclosure, strengthens the system construction of private equity information disclosure, and regulates the content and methods of private equity fund information disclosure obligors to disclose to investors. Significance: It is conducive to protecting the right to know of private equity investors, thereby protecting the legitimate rights and interests of private equity investors and promoting the rational allocation of market resources. 6. Announcement on Further Regulating Certain Issues Concerning the Registration of Private Equity Fund Managers Promulgated by the Fund Industry Association on February 5, 2016 Key points: (1) Cancel the registration certificate of the private fund manager. (2) Private placements shall promptly file products, perform information reporting obligations and submit audited annual financial reports on time. (3) Legal opinions must be submitted for new applications for private placement, first-time filing of products, or major event changes. (4) It is stipulated that private equity executives should obtain the qualifications for fund employment. (5) The registered private placement manager will not be disqualified for the products that are not filed. Significance: It means the tightening of the private placement filing, and the cancellation of the “empty shell†private placement action on May 1 and August 1 effectively purifies the industry air. 7. "Management Measures for the Raising of Private Investment Funds" Promulgated by the Fund Industry Association on April 15, 2016 Key points: (1) Private equity fund raising entity qualifications are only those that register private equity and obtain fund sales qualifications. (2) The raiser assumes the responsibility of identifying and identifying qualified investors. (3) The fundraising institution and the supervisory bank shall sign a supervision agreement. (4) Private placements may not publicly promote products and performance. (5) Private product promotion must be targeted to specific targets. (6) To be confirmed by qualified investors, illegal split transfer is prohibited. (7) Implement a 24-hour investment cooling-off period and confirm the return visit system. Significance: The “Management Measures for Recruitmentâ€, as a new regulation for private equity self-discipline, clarifies various aspects of the private placement process, is the first line of defense against the risk of non-compliance, and guides the fundraising institutions to legally operate in compliance, thus self-discipline in the private equity industry in China. The rules system is gradually taking shape. The association takes self-discipline rules as the starting point, and through continuous registration, classification, publicity inspection, disciplinary action, blacklisting and information sharing, it constantly improves and strengthens the self-regulatory mechanism afterwards and guides the private equity industry. Honest and trustworthy, compliant operation, win the trust of investors, win the recognition of the society and capital market, and win the foundation. 8. The regulatory layer hopes to form a complete system of self-regulatory rules that regulates the development of the private equity industry, including: "7 ways" Amendments to the Measures for the Administration of Registration of Private Equity Funds "Management Measures for the Raising of Private Equity Funds" has been released "Private Fund Information Disclosure Measures" has been released The “Management Measures for Private Equity Fund Managers Engaged in Investment Consultancy Business†The “Management Measures for Private Equity Custody Business†was formulated and improved. The “Management Measures for Private Equity Outsourcing Service Business†was formulated and improved. The Fund Management Qualification Management Measures are formulated and improved. "2 guidelines" "Private Fund Contract Content and Format Guidelines" has been released "Guidelines for Internal Control of Private Equity Funds" has been released 9. The State Council's "Regulations on the Management of Private Equity Investment Funds" was introduced during the year. On April 13, 2016, the Chinese government website announced the notice of the State Council's 2016 legislative work plan, requiring the CSRC to draft the Regulations on the Management of Private Equity Investment Funds, and was listed as a project that is urgently needed to comprehensively deepen the reform. Private equity development trend 1. Close to the public offering scale, the amount of private placement brings a tipping point Since the launch of the private placement filing in 2014, we can see that the industry is developing very fast. According to the data, as of the end of July 2016, there were 16,500 registered private equity managers, and the number of privately-distributed products was 36,800, the subscription volume was 7.47 trillion yuan, and the paid-up scale was 6.11 trillion yuan. Compared with public offerings, fund companies manage public fund levels of 7.95 trillion yuan. It can be seen that the total size of private placements is close to the total size of public offerings, and the explosive growth of private placements is evident. At the same time, the industry-represented tens of billions of private-equity aircraft carriers have reached the growth of 131 large-scale private equity asset management companies, which means that private equity has become a force that cannot be ignored in the asset management industry. 2. The industry is ruled by chaos, taking the normative development path In the process of development and growth, the private equity industry has exposed many problems. Some institutions, in the name of private placements, illegally self-increasing letters with the registration and filing information of the association, engaging in illegal fund-raising and other illegal activities, and concurrently engaging in non-private partnerships such as P2P, private lending, and guarantees. The business has caused major infringements on the interests of investors and has also discredited the image of the private equity industry. The CSRC said that the current risk of illegal fund-raising in the private equity industry is outstanding. Since 2014, there have been many illegal fund-raising cases in the name of private equity funds, involving 32 registered institutions, 5.9 billion yuan of private equity funds have been filed, and tens of thousands of investors. Under the guidance of the China Securities Regulatory Commission, starting from the second half of 2015, the China Securities Investment Fund Association began to formulate a number of heavyweight policies, which opened the prelude to the regulation of the private equity industry. At present, the supervision mainly includes several aspects. First, starting from the basic filing work, through the introduction of the legal opinion system, requiring the senior executives to obtain the qualifications for the fund, etc., to lay the basic practice norms of the private equity industry; second, set up a set of “7 +2" self-discipline rules system, from the internal control, information disclosure, recruitment behavior and other aspects to regulate private equity behavior, strengthen post-event supervision; Third, establish a private equity failure system, classified publicity system, etc., while combating private equity violations Fourthly, while regulating private equity as a manager's business, the private equity as a business model of investment is also included in the supervision. The provisional provisions of the securities and futures asset management regulations on third-party investment qualifications, etc., to prevent business risks and avoid Regulatory arbitrage. At the same time, the association also carried out two stages of “empty shell†private placement cancellation work, and more than 10,000 institutions have been registered as private equity managers. 3. Hedging tools are still restricted At present, the mainstream private equity strategies in the market include several major strategies: common stock strategy, bond strategy, market neutrality, arbitrage strategy, macro hedging, management futures, private placement, and portfolio funds. Private equity investment is moving from purely active management to stock selection to quantification and hedging. At the same time, however, there are fewer hedging instruments available for private placement. After the stock market crash in 2015, there are more restrictions on the use of stock index futures. In addition, many derivatives hedging instruments such as options are still to be developed and used. There are still hedge funds in the true sense. distance. 4. Private placements have broken public offerings but the details remain to be determined At the end of June 2016, Yang Aibin, the former investment director of China Huaxia Fund, finally won the public offering approval and established the public fundraising Pengyang Fund, becoming the first “private public†investor. Private placements apply for public offerings, and require private management companies' management systems, product lines, risk control processes, and talent teams. They also involve the integration of existing private equity services and the establishment of a firewall system. Since the new "Fund Law" promulgated by the China Securities Regulatory Commission in 2013 and the "Interim Provisions on the Establishment of Public Fund Management Business by the Asset Management Organization", there is no policy obstacle for private equity to enter the public fundraising gate. However, after the private placement of public funds, how to deal with the original private equity business, how to establish a public and private recruitment firewall system to prevent interest transmission and conflict, still need to be further clarified. 5. Accelerating the layout of overseas globalization has opened In the context of the globalization of China's capital market, the pace of private equity entering the overseas market is accelerating. In the past few years, there have been freshwater spring investment, Jinglin assets, investment in the heart of Chizi, and thousands of joint ventures to set up companies in Hong Kong, investing overseas and raising capital, etc., as well as privately-owned overseas products such as Yuanle’s assets and Dingfeng assets. , investing in Hong Kong stocks, China stocks, etc. Recently, private equity has accelerated the pace of going to sea, and Chongyang Investment, Fushan Investment, Shenzhou Mud Fund, Wangzheng Capital and other private placements have once again made a splash. Entering overseas markets has also become one of the important directions for the development of private equity. There are two main forms of domestic private placements that currently carry out overseas business. One is to register funds directly in the Cayman Islands and other places to be responsible for investment; the other is to apply for a capital management license in Hong Kong and set up a company investment. In terms of investment varieties, the company actively manages private placements to invest in China stocks and participates in overseas high-yield bonds; quantitative private placements mainly involve commodity futures, stock index futures, stocks, etc.; in terms of funds, some are raised in China and passed through qualified domestic territory. Institutional investors (QDII) invest in overseas products, and some directly raise overseas. 6. Private equity embraces the new three board equity investment prospects In the past few years, Sunshine Private Equity, which has been developed in the secondary market of stocks, has begun to focus on the broader New Third Board market and has started equity investment. Shanghai Chengrui Investment, Shanghai Dingfeng Assets, Shanghai Zhuque Investment, Beijing Heju Investment, Beijing Shennong Investment, etc. are all investing in the large-scale private equity of the New Third Board. They set up special equity investment companies or departments and teams to issue new three boards. Investment funds have made great strides in the equity market. 7. Capital source diversified institutional funds led to private placement At the beginning of its establishment, private placements mainly focused on self-owned funds and retail funds. However, in recent years, banks, trusts and other institutions have begun to favor private equity institutions and hand over their money to private placements, especially since 2016. Under the background of asset shortage, the willingness to allocate funds from institutional funds represented by bank subcontracting funds is very strong. Private equity also hopes to match this part of the funds. Currently, fund industry associations and other institutions are actively promoting this matter. However, as a private equity fund with a very large amount of private placements, it is difficult to get favored by institutions with low risk appetite such as subcontracting funds. Only some private placements with good performance, stable style and complete control over the years can get the funds of the institutions. Therefore, how to design a product and investment form suitable for the organization in the future, form a stable investment style, and become the key to the funds of the private placement agency. Report Writer: China Fund Reporter Wu Jun Enter [Sina Finance and Economics Unit] Discussion Microfiber Spa Robe,Microfiber Bathrobe,Microfiber Bath Robes,Microfiber Travel Bathrobe Wujiang Rongchao Silk Co., Ltd , https://www.wujiangrongchao.com